Overview

Israeli consumers are sophisticated and enjoy diverse food tastes. Currently, over 18% of household expenditures are dedicated to food products. The agro-food sector is well-developed, encompassing producers, food processors, wholesalers, retailers, food service operators, and importers. This dynamic domestic market is competitive but heavily reliant on imports due to limited arable land and fresh water suitable for agriculture.

The Ministry of Agriculture and Food Security is leading a 25-year food security initiative aimed at addressing these challenges. The program focuses on enhancing agricultural technology, expanding water desalination projects, and fostering international partnerships to ensure long-term food security. Despite these efforts, Israel remains dependent on imports for key agricultural products, including feed grains, sugar, rice, and milling wheat.

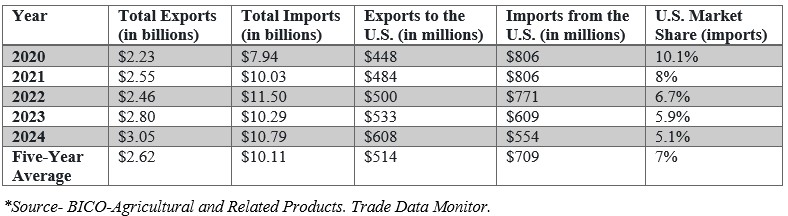

In 2024, imports of agricultural and related products reached $10.8 billion, with approximately 5.1% sourced from the United States. However, Israel’s limited land and water resources, combined with reliance on foreign agricultural workers, continue to drive up local production costs and consumer prices. For example, while poultry meat is sourced domestically, nearly all feed for poultry and egg production is imported, leaving prices vulnerable to global market fluctuations.

Table: Israel’s Agricultural Trade (USD)

Israel posts significant trade deficits in food and agricultural products. The country imports large volumes of feed grains, sugar, rice, and milling wheat, as well as consumer-oriented agricultural products to meet nutritional demands. Below is a summary of Israel’s agricultural trade over the past five years:

The Israeli food processing industry is a key player in the domestic economy, with over 2,500 facilities, generating annual revenues of $13.65 billion in 2023 for the 10 largest food companies. The Israeli food processing industry is highly innovative, introducing new products and adopting advanced production technologies. Major multi-national food manufacturers such as Nestlé, Unilever, Danone, and Pepsi Co. collaborate with leading Israeli companies such as Osem and Strauss. Four groups dominate the local food processing industry: Tnuva, Osem-Nestlé, Unilever, and Strauss.

With limited land and resources, the growing population drives demand for imported food ingredients, creating opportunities for U.S. exporters. The EU is the largest trade partner (as a union) of Israel, and on January 1, 2025, the Israeli Ministry of Health adopted EU food standards under the legislation “What is good for the EU is good for Israel.” Transition periods for compliance are expected to last several years and may affect U.S. food exporters, especially those which currently do not export their products to the EU.

Israeli Fast Moving Consumer Goods (FMCG) sales reached $16.02 billion in 2023, with $12.9 billion attributed to food and beverages. The food retail market is made up of supermarket chains, convenience stores, open markets, and neighborhood grocery stores. Sales in supermarket chains account for most of the retail food market sales. Large supermarket facilities are in the outskirts of the large cities near major roads and tend to be cheaper than smaller neighborhood stores. Smaller neighborhood supermarkets are conveniently located but tend to be more expensive, with a smaller variety of products.

U.S. products are not always competitive due to relatively higher production and freight costs. Products from Europe, the Mediterranean Basin and the Black Sea Basin have an advantage due to proximity and, in some cases, lower production costs. Transportation costs are less impactful for products with a high value-to-volume ratios, such as spices, essences, flavorings, and concentrates. Similarly, U.S. products eligible for tariff preferences under the United States-Israel Agreement on Trade in Agricultural Products (ATAP) are advantaged, making transportation costs less of a factor.

The Israeli food and food supplement legislation and standardization system is increasingly harmonized to European standards. In many cases, European standards may differ from those in the United States, resulting in non-tariff trade barriers and a challenging import licensing process.

Shipping costs have risen periodically in recent years, mainly due to higher insurance costs attributed to geopolitical and logistical challenges and the increase in world shipping prices. Air cargo shipping prices surged in 2024 due to reduced airline capacity following the war. Combined with global commodity price increases and higher domestic production costs, these factors have led to significant food price inflation in Israel.

Kashrut

Exporters should consider the issue of kashrut or kosher certification. Kosher certification is not a legal requirement for importing food into Israel, except for beef, poultry, and other meat products. However, non-kosher products have a smaller market share, as most supermarkets and hotels refuse to carry them. In recent years there has been an increase in demand for non-kosher foods, or foods that lack kosher certification, especially from the former Soviet Union diaspora.

Manufacturers who produce kosher products must be able to satisfy Israeli rabbinical supervisors’ demands that all ingredients and processes meet kosher standards. According to the Law for Prevention of Fraud in Kashrut, only the Chief Rabbinate of Israel can approve a product as kosher for consumption in Israel. The Chief Rabbinate may also authorize another supervisory body to act on his behalf; the kashrut certification issued by many U.S. rabbis is recognized by Israel’s Chief Rabbinate. Israeli importers can also send an Israeli rabbi to any supply source to certify the products.

Prohibited Imports

Israel, a member of the World Trade Organization (WTO), maintains relatively few prohibitions on agricultural imports. However, Israeli authorities prohibit the import of non-kosher meat and meat products (including beef, poultry, and mutton) under the Law for Prevention of Fraud in Kashrut which requires these imported products to be certified as kosher by the Chief Rabbinate of Israel. These regulations do not apply to other non-kosher animal products such as shellfish. The only other product prohibitions are targeted against internationally controlled substances or are designed to protect human, animal or plant health, or national security.

The U.S.-Israel Free Trade Agreement allows both countries the use of non-tariff restrictions and prohibitions on products from those agricultural subsectors that are sensitive to agricultural policy shifts. Israel has removed some administrative barriers for United States imports but retains high levies on products and commodities that compete with the local industry, such as dairy, apples, and wine.

Resources

- Central Bureau of Statistics (CBS), Israel

- Standards Institution of Israel (SII)

- USDA-FAS GAIN Reports

- Plant Protection and Inspection Services | Ministry of Agriculture and Food Security

- משרד החקלאות וביטחון המזוןMinistry of Agriculture and Food Security (MoAFS)

- Food Control Service, Ministry of Health

Post Contact and Additional Information

USDA-FAS, Office of Agricultural Affairs, U.S. Embassy Jerusalem, Tel-Aviv Embassy Branch

Tel: +972-3-519-8667

E-mail: agtelaviv@usda.gov